The global oil market is currently operating under a fundamental decoupling of announced production quotas and actual marginal price drivers. While OPEC+ has signaled a strategic pivot toward increasing output, the upward trajectory of crude prices persists because the market has priced in a structural inability to meet these targets. To understand why oil prices climb in the face of nominal supply increases, one must look past the press releases and analyze the physical constraints of the global energy supply chain and the shifting risk premiums in the Middle East and Eastern Europe.

The Three Pillars of Artificial Scarcity

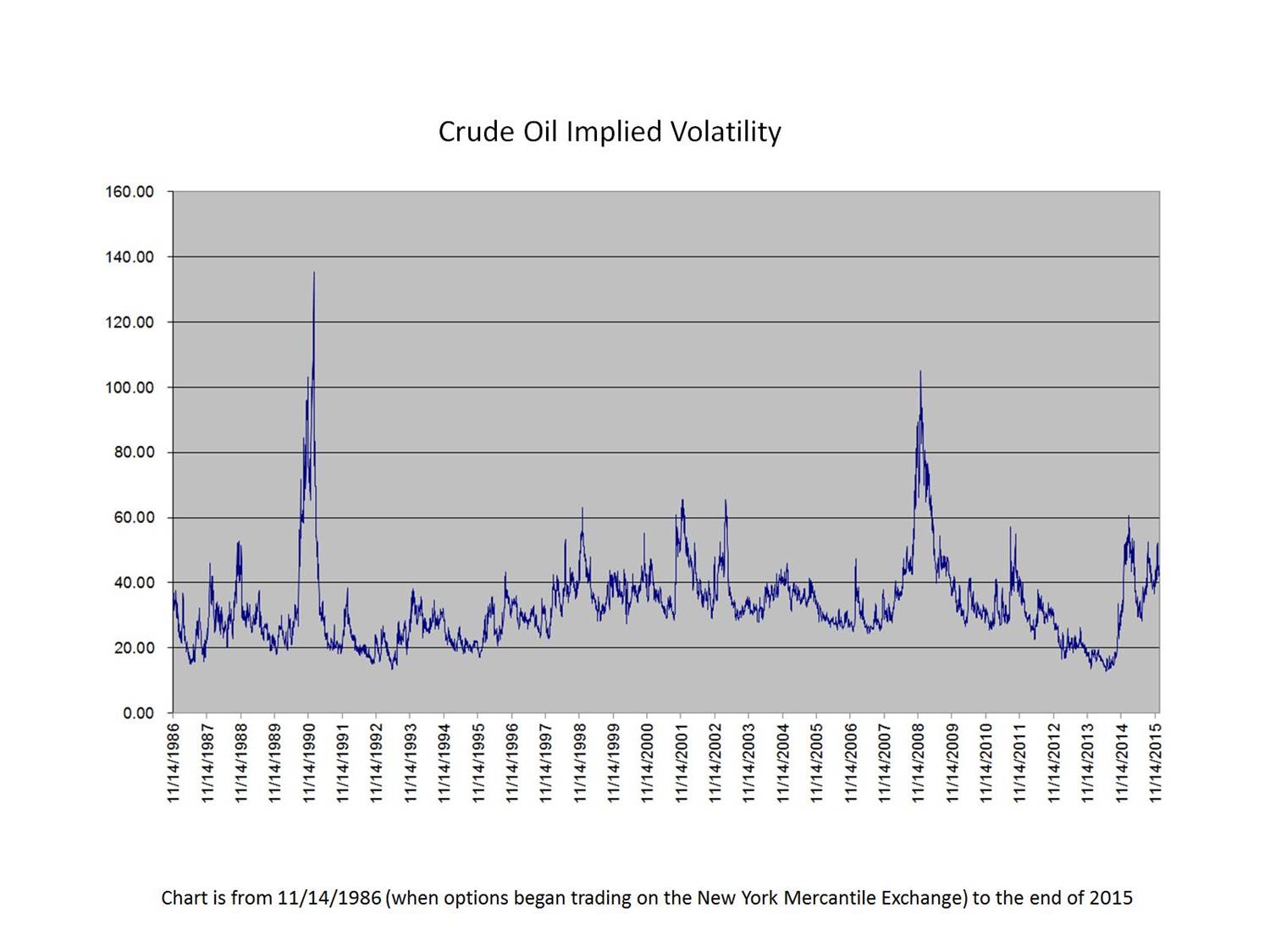

The current pricing environment is not a reaction to a lack of resources, but a reaction to the narrowing of the global "buffer." This buffer—composed of spare capacity, inventory levels, and logistical flexibility—is being eroded by three distinct factors that render OPEC+ announcements secondary to market reality. For an alternative look, see: this related article.

1. The Spare Capacity Illusion

Market analysts frequently mistake "paper capacity" for "effective capacity." While the OPEC+ alliance claims the ability to bring millions of barrels back to the market, the actual volume of high-quality, light-sweet crude that can be mobilized within a 30-to-90-day window is significantly lower. Chronic underinvestment in upstream infrastructure among secondary members (specifically within the African and Central Asian blocs) has led to a natural decline in wellhead pressure and facility integrity. When these nations are "allowed" to produce more, they often find their physical systems cannot sustain the higher flow rates, resulting in a persistent production gap.

2. The Geopolitical Risk Transference

Traditional energy models often treat geopolitical tension as a binary "on/off" switch. Modern markets, however, view it as a continuous cost of insurance. Even as supply targets rise, the threat of maritime disruptions in the Strait of Hormuz or drone strikes on refining infrastructure in the Black Sea adds a permanent $5 to $10 "security premium" per barrel. This premium is inelastic; it does not disappear when production quotas are lifted. In fact, higher production targets can exacerbate this risk by increasing the volume of oil in transit through contested chokepoints, thereby increasing the potential impact of any single disruption. Further coverage on this matter has been provided by Forbes.

3. The Refined Product Bottleneck

Crude oil price is increasingly a function of "crack spreads"—the difference between the price of a barrel of crude and the petroleum products extracted from it. Global refining capacity has not kept pace with crude production capabilities. We are currently facing a "geometry problem" where the world has plenty of heavy sour crude, but limited capacity to turn it into the ultra-low sulfur diesel and jet fuel the global economy demands. Even if OPEC+ floods the market with raw crude, the price of the final energy unit remains high because the conversion process is at maximum utilization.

The Cost Function of Energy Transition Uncertainty

A primary driver of price resilience is the "Investment Paralysis Loop." Integrated oil companies (IOCs) and national oil companies (NOCs) are caught between immediate demand signals and long-term decarbonization mandates. This creates a specific cost function that favors high prices over volume growth.

- Capital Discipline as a Defense Mechanism: Shareholders now demand dividends and buybacks over exploration and production (E&P) expansion.

- Regulatory Friction: Increased environmental, social, and governance (ESG) scrutiny has raised the "hurdle rate" for new projects. A project that was viable at $60/barrel in 2015 now requires $85/barrel to account for the risk of "stranded assets" in a net-zero future.

- The Technical Talent Deficit: A decade of shifting away from fossil fuels has led to a brain drain in petroleum engineering. The human capital required to rapidly scale up production is no longer as mobile or abundant as it was during the shale revolution of 2010–2014.

Dissecting the Inventory Lag

Inventories serve as the shock absorbers of the global economy. Standard economic theory suggests that if OPEC+ increases output, inventories should rise and prices should fall. This logic fails to account for the "Re-stocking Threshold."

OECD commercial stocks are currently hovering near five-year lows. At these levels, any incremental barrel added to the market is immediately diverted into primary storage rather than being traded on the spot market. This creates a psychological floor for prices. Traders recognize that for the next 12 to 18 months, every "extra" barrel is spoken for by strategic and commercial reserves looking to buffer against future shocks. The market remains in "backwardation"—a state where the current price is higher than the future price—signaling that immediate delivery is still valued far more than long-term supply security.

The China Demand Variable: A Latent Force

The assumption that high prices will lead to immediate demand destruction is flawed in the context of emerging markets, particularly China and India. These economies are in a phase of intensive industrialization where energy intensity per unit of GDP remains high.

China’s move toward "energy independence" involves massive stockpiling of crude, regardless of the price. This non-commercial demand creates a baseline of buying activity that ignores the traditional price-demand curve. When OPEC+ announces a production increase, these state-backed entities often use the resulting minor price dips as entry points to increase their long-term reserves, effectively neutralizing the intended downward pressure on the market.

The Mechanics of the Shale Ceiling

For years, US Shale was the "swing producer" that could break OPEC's grip. That era has ended. The US shale industry has transitioned from a growth-at-all-costs model to a "value-over-volume" strategy.

$$P_{break-even} = \frac{C_{opex} + C_{capex} + R_{required}}{V_{total}}$$

The variables in this equation have shifted. Operating expenses ($C_{opex}$) are rising due to labor and equipment inflation. The required return ($R_{required}$) has spiked as investors no longer tolerate the debt-fueled drilling of the past. Consequently, US production is no longer a reactive force that can flood the market the moment prices tick upward. The "Shale Ceiling" is now a rigid structural limit, leaving OPEC+ as the only entity with the keys to the engine room—and they are turning the keys very slowly.

Strategic Friction in the OPEC+ Alliance

The internal logic of OPEC+ is not a monolith; it is a delicate balance of competing national interests. Saudi Arabia requires a specific price point to fund its "Vision 2030" economic diversification. Russia requires high energy revenues to sustain its geopolitical maneuvers. These fiscal break-even prices are significantly higher than the actual cost of extraction.

When the alliance announces a "pledge to raise output," it is often a political maneuver to appease Western consuming nations rather than a genuine commitment to lowering prices. The strategy is to increase volume just enough to prevent a global recession, but not enough to erode the per-barrel profit margin. This "Goldilocks Pricing" strategy ($85–$100 range) is the true objective, and the market knows it.

The Logistics of Displacement

Even if production increases, the global tanker fleet is facing its own constraints. The "shadow fleet" used to transport sanctioned oil has diverted hundreds of vessels from the standard shipping routes. This has increased ton-mile demand and pushed charter rates to historic highs.

The physical cost of moving oil from the Persian Gulf to North America or Europe has effectively doubled in the last 24 months. These logistical costs are baked into the final price at the pump or the factory gate. An increase in OPEC+ production actually increases the demand for tankers, which can further drive up shipping costs, creating a circular inflationary effect on the final landed price of crude.

Quantitative Analysis of Current Price Support

The upward pressure on oil is sustained by a convergence of three specific data points:

- Low Spare Capacity: Global spare capacity is estimated at less than 2% of total demand. In a 100-million-barrel-per-day market, a 2-million-barrel disruption (roughly the output of Kuwait) would leave the world with zero margin for error.

- The Dollar-Oil Inverse Correlation Weakening: Historically, a strong US dollar suppressed oil prices. Recently, we have seen both a strong dollar and high oil prices—a rare signal that the underlying commodity scarcity is overmatching currency fluctuations.

- The Capex Gap: Cumulative underinvestment in global upstream projects since 2014 has reached an estimated $600 billion. This is not a gap that can be closed by a simple policy shift; it requires years of physical construction and drilling.

The path forward for energy markets is one of "constrained volatility." The baseline for crude has structurally shifted upward. Investors and corporate strategists should discard the expectation of a return to the $50–$60 range in the near term. Instead, the focus must shift to hedging against a permanent $90+ environment where supply announcements are treated as noise and physical "barrels in hand" are the only true currency.

To mitigate the impact of this regime shift, downstream entities must prioritize energy efficiency gains and feedstock flexibility. Relying on OPEC+ to "save" the market through volume increases is a fundamental misunderstanding of the alliance's fiscal needs and the physical reality of the world's aging oil fields. The strategic play is to assume that the supply pledge is a ceiling on production, not a floor for prices.