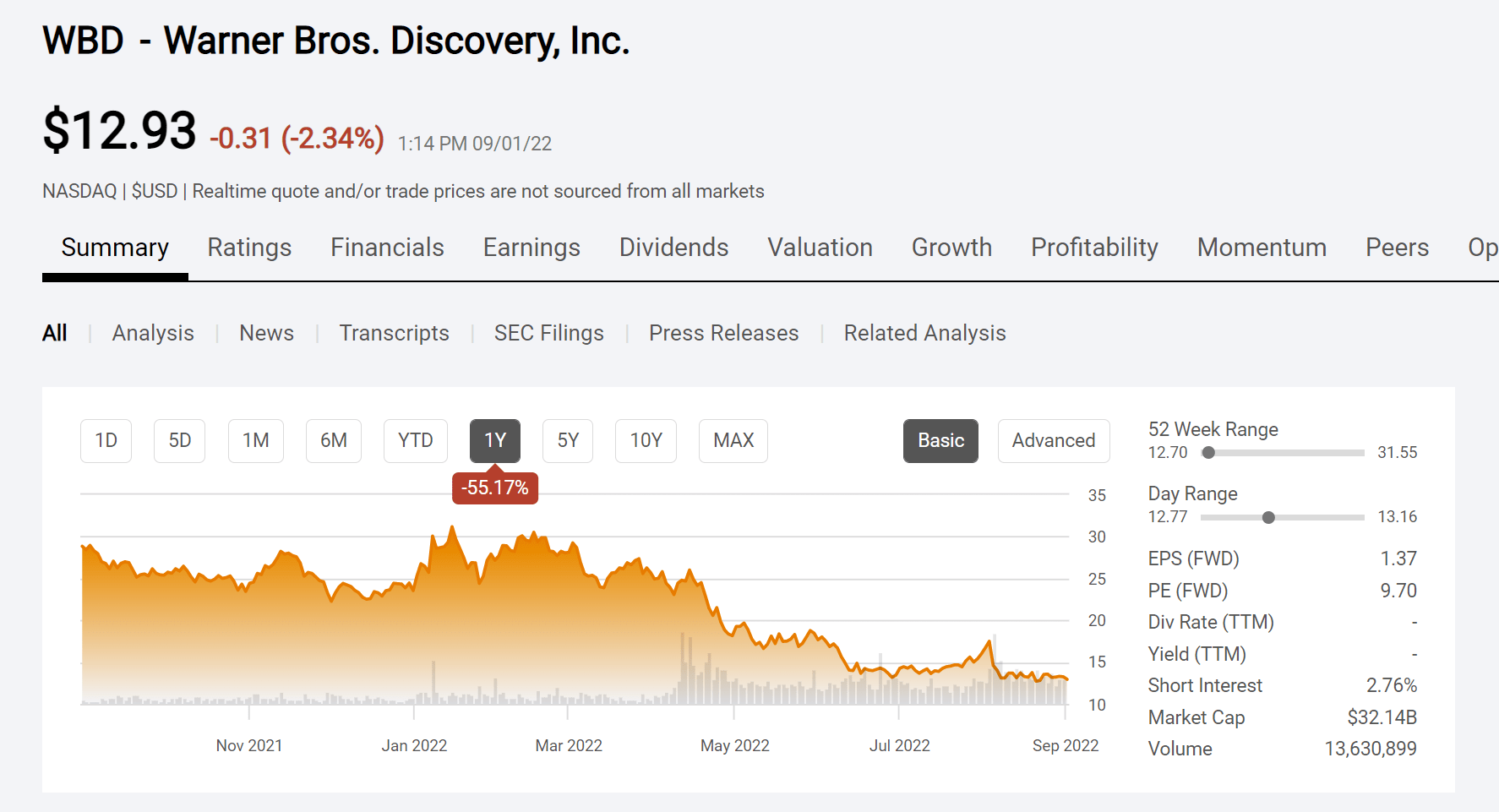

The fate of Warner Bros. Discovery (WBD) is not a question of creative output or brand prestige; it is a mathematical certainty dictated by the divergent physics of legacy linear cash flows and the capital intensity of direct-to-consumer (DTC) scaling. While public discourse focuses on who might buy the studio, the actual strategic bottleneck is the structural incompatibility of WBD’s debt profile with its long-term growth requirements. The current entity exists in a state of managed decline, where the primary objective is not expansion, but the extraction of sufficient EBITDA from a dying cable ecosystem to service a $40 billion debt load before the underlying asset evaporates.

The Linear Decay Function

To understand why WBD is an inevitable acquisition target, one must quantify the velocity of the "Linear Cliff." The company’s core problem is the disproportionate reliance on linear networks (CNN, TNT, TBS, Discovery) to fund its streaming aspirations.

- The Affiliate Fee Feedback Loop: As cord-cutting accelerates, the subscriber base for cable networks shrinks. This reduces the total pool of affiliate fees—the high-margin revenue that previously subsidized prestige content.

- Ad-Revenue Compression: Reduced viewership leads to lower ratings, which triggers a downward spiral in CPM (cost per mille) rates. Advertisers are shifting budgets to platforms with superior deterministic data, such as YouTube or Netflix’s nascent ad tier, leaving WBD fighting for a shrinking slice of the traditional TV ad market.

- The Sports Rights Inflation: WBD’s recent loss of the NBA broadcasting rights is not merely a programming failure; it is a structural blow to the company’s leverage. Without "must-have" live sports, WBD’s ability to demand high carriage fees from distributors like Comcast or Charter vanishes.

The result is a negative compounding effect. The cash generated by these networks—previously the "engine room" of the business—is decelerating faster than the Max streaming service can scale to replace it.

The Three Pillars of Media Consolidation

The strategic logic for a WBD sale or merger rests on three distinct pillars of industrial necessity. Any potential suitor must solve for at least two of these to justify the regulatory scrutiny and capital expenditure required for a takeover.

I. The Scale Threshold

In the global streaming war, the minimum viable scale is no longer domestic; it is planetary. Netflix and Disney operate at a scale where the marginal cost of adding a subscriber is negligible compared to the lifetime value (LTV) generated. WBD, despite the quality of the HBO library, remains in a middle-ground purgatory. It is too large to be a niche player but lacks the distribution infrastructure to compete with the "Big Tech" entrants (Apple, Amazon, Google). An acquirer provides the plumbing—the global billing systems, hardware integration, and cloud infrastructure—that WBD cannot afford to build while paying down its debt.

II. IP Maximization and Vertical Integration

The Warner Bros. film studio is a factory for "Systemic IP." This refers to franchises (DC, Harry Potter, Dune) that can be monetized across multiple windows: theatrical, SVOD, gaming, and consumer products. The inefficiency of the current WBD structure is that it lacks the flywheel of a Disney or a Universal. It does not have the theme park footprint of Comcast/NBCUniversal nor the retail ecosystem of Amazon. Ownership by an entity with a diversified revenue model allows the IP to be "loss-leaders" for more profitable segments, rather than forcing every individual film to carry the burden of the corporate interest payments.

III. The Cost of Capital Arbitrage

WBD’s enterprise value is suppressed by its debt-to-equity ratio. A suitor with a stronger balance sheet (e.g., Apple or a consolidated NBCUniversal/WBD entity) can refinance or absorb this debt at lower rates. The "Ownership Question" is fundamentally a search for a lower cost of capital. The current management is forced to cut costs—often at the expense of long-term brand equity—simply to keep the lights on. A new owner resets the clock.

The Probability of Acquisition Pathways

Strategic analysis of the marketplace reveals a limited set of viable exits. Each carries distinct regulatory and operational risks that define the eventual price point.

- The NBCUniversal Merger (Comcast): This is the most logical operational play. The combination of Universal and Warner Bros. would create a studio powerhouse capable of rivaling Disney. It merges the peacock and Max platforms, achieving massive overhead reduction. However, the regulatory environment in the United States currently views such "horizontal" mergers with extreme skepticism. The Department of Justice (DOJ) would likely demand the divestiture of major cable assets or news divisions (CNN/MSNBC), which complicates the deal math.

- The Big Tech Absorption (Apple/Amazon): For Apple, WBD is a content shortcut. Apple TV+ has prestige but lacks the deep library necessary to prevent churn. Buying WBD would give Apple 100 years of cinema history and a turnkey production engine. The barrier here is cultural and financial; Big Tech firms are hesitant to take on the "toxic" declining assets of linear television that come attached to the WBD studio.

- The Private Equity Breakup: If a strategic buyer does not emerge, the most likely outcome is a "Sum of the Parts" liquidation. This involves spinning off the Max/HBO/Studio business into a "GrowthCo" and leaving the linear networks in a "DebtCo" to be milked for cash until they are insolvent. This creates value for shareholders but destroys the integrated power of the original brand.

The "Max" Paradox: Why Growth Isn't Enough

Management frequently points to the global rollout of Max as the solution. However, the unit economics of streaming suggest a "Subscription Trap."

$Profit = (Subscribers \times ARPU) - (Content Spend + Marketing + Churn)$

For WBD to reach a terminal state of profitability, it must increase ARPU (Average Revenue Per User) without triggering a mass exodus (Churn). This is nearly impossible when competitors like Netflix have higher engagement metrics. WBD is trapped in a cycle where it must spend billions on "tentpole" content just to keep its current audience, leaving no excess capital to pay down the principal on its debt.

Furthermore, the "Great Unbundling" has shifted the power back to the consumer. In the cable era, customers paid for WBD content whether they watched it or not. In the streaming era, they can cancel with a single click. This volatility makes the cash flows from WBD's streaming arm significantly less predictable—and therefore less valuable—than the legacy fees they are replacing.

Operational Bottlenecks in the Search for a Buyer

Potential acquirers are currently observing WBD through the lens of the "Falling Knife" principle. The longer they wait, the lower the valuation might drop as the linear business erodes.

- The CNN Problem: CNN is a prestigious asset but a regulatory nightmare. Any buyer (especially a foreign one or a tech giant) would find the political scrutiny attached to owning a major 24-hour news network to be a liability rather than an asset.

- The DC Studios Gamble: The valuation of the DC Universe is currently speculative. If the upcoming James Gunn-led slate fails to reach Marvel-level box office consistency, the projected "long-tail" value of the WBD library drops significantly.

- The Gaming Division: WBD owns world-class gaming studios (Rocksteady, NetherRealm). While highly profitable, this is a volatile hit-driven business that requires constant reinvestment. A buyer like Microsoft or Sony would value this segment highly, but a traditional media company might see it as an unnecessary complexity.

The Impending Strategic Pivot

The ownership of Warner Bros. Discovery matters because the current corporate structure is a transition state, not a destination. The company is currently "dressed up for sale." Every cost-cutting measure, every shelved film project, and every licensing deal (such as putting HBO content on Netflix) is an attempt to optimize the balance sheet for a 2025-2026 transaction window.

The industry is moving toward a "Three-Player Market" where only three global platforms will have the scale to survive: Netflix, Disney, and a third, yet-to-be-finalized entity formed from the remnants of WBD, Paramount, and potentially NBCUniversal.

The strategic play for investors and industry observers is to ignore the noise of quarterly "subscriber additions" and focus on the Free Cash Flow to Debt Ratio. Once the decline in linear EBITDA exceeds the growth in DTC EBITDA for three consecutive quarters, the board will be forced to trigger a sale regardless of the regulatory environment. The "Who" of the ownership matters less than the "When," as the price will be dictated by the desperation of the seller rather than the ambition of the buyer.

Warner Bros. Discovery is essentially a library of the 20th century’s greatest stories, currently being used as collateral for a 21st-century debt crisis. The eventual owner will be the entity that can decouple those stories from the dying delivery mechanisms of the past. For WBD to survive, it must stop being a media company and start being a subsidiary of a platform company.

The final move will likely involve a tax-efficient spin-merge, separating the "dead" linear assets into a standalone entity, allowing the Studio and Max to merge with a healthier partner. This "Reverse Morris Trust" style maneuver is the only way to shed the debt burden and allow the HBO brand to return to its primary function: the creation of cultural capital, rather than the servicing of interest payments.

The Immediate Strategic Play

Expect a proactive divestiture of non-core assets—specifically the gaming division or a minority stake in the film library—within the next 18 months. This is a pre-emptive strike to reduce the "complexity discount" that currently plagues the stock price. Any entity looking to acquire WBD will demand a cleaner organization. Therefore, the internal mandate will shift from "growth at all costs" to "asset purification." The goal is no longer to win the streaming war, but to be the most attractive target left on the battlefield.