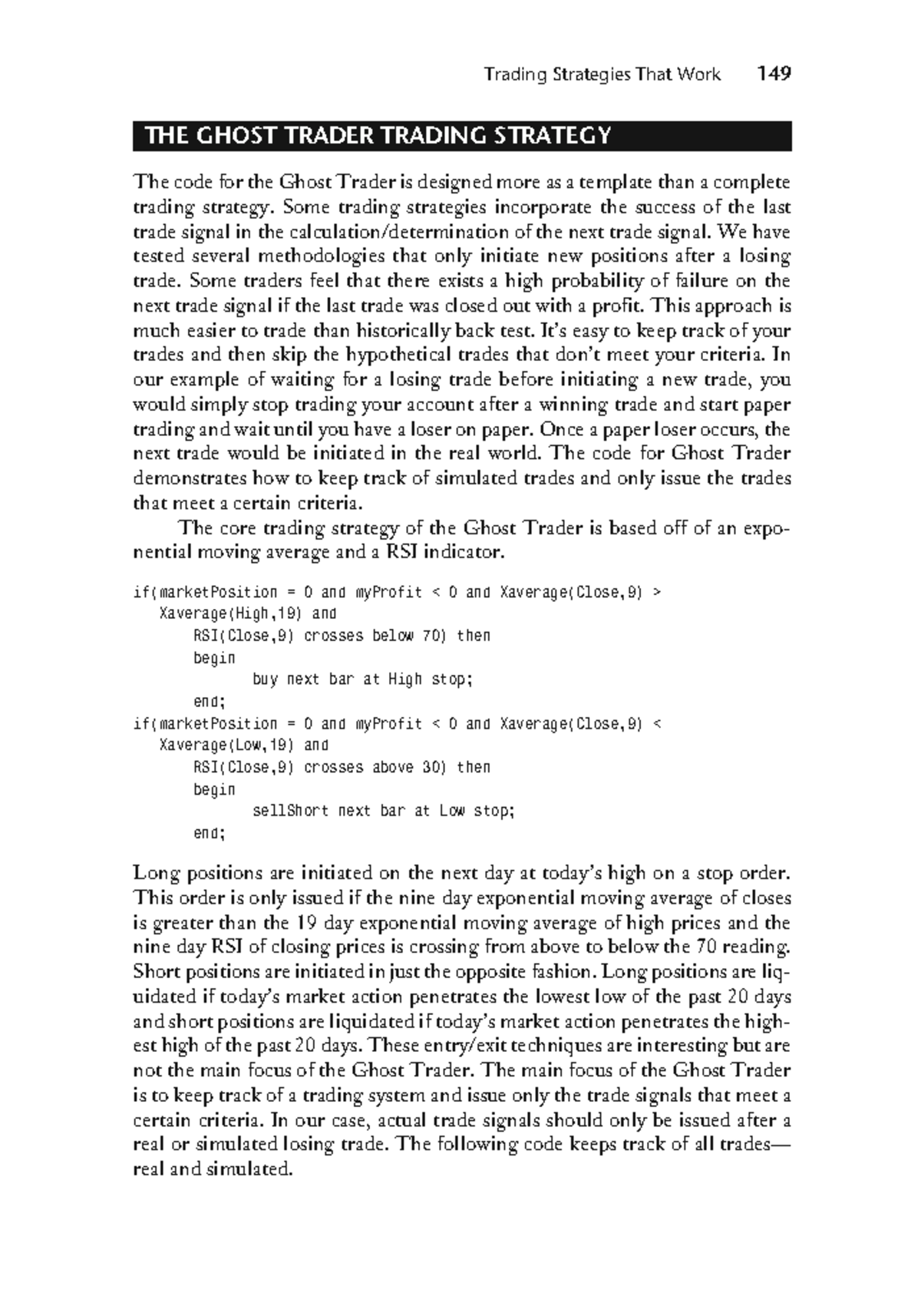

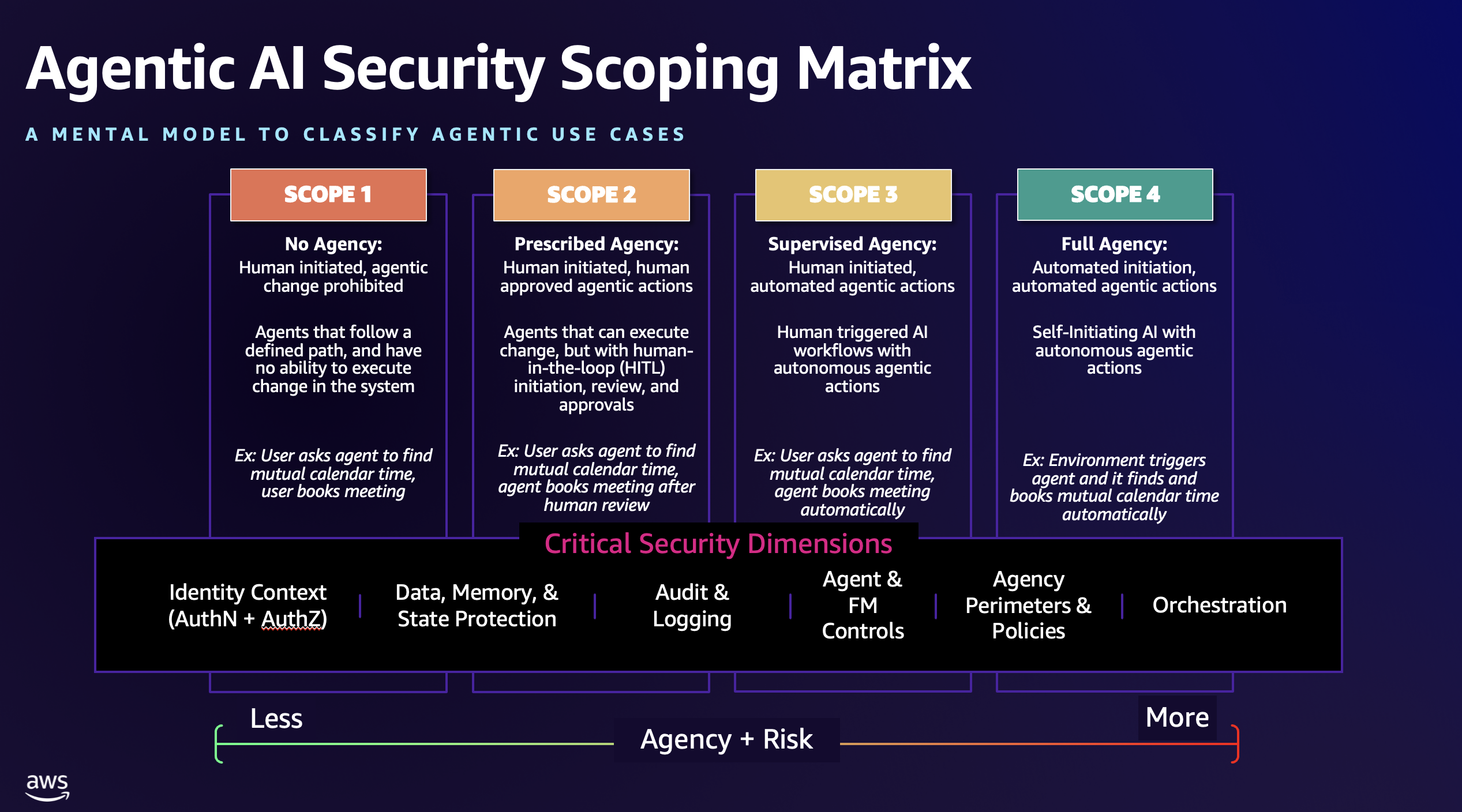

The software-as-a-service gold rush is over. For a decade, the playbook was simple: acquire users, raise prices, and let the "sticky" nature of enterprise platforms guarantee perpetual growth. Wall Street rewarded this with eye-watering valuation multiples, often treating a 30% revenue growth rate as a divine right. But in early 2026, the floor fell out.

The catalyst wasn’t a single earnings miss. It was a realization. Investors are finally acknowledging that the very artificial intelligence meant to "supercharge" these platforms might actually be the thing that dismantles their business models. As bellwethers like Salesforce, Adobe, and ServiceNow see their market caps shaved by billions, the narrative has shifted from "AI as an add-on" to AI as an existential threat.

The Death of the Per-Seat Tax

For years, the software industry lived on the "seat-based" model. You paid for every human employee who logged into the system. It was a highly predictable, incredibly lucrative tax on headcount.

Generative AI has broken this logic. When an AI agent can do the work of five junior analysts, a company no longer needs five seats of a Customer Relationship Management (CRM) tool. They need one. The efficiency gains that AI delivers to the end-user are, ironically, a direct drain on the software vendor’s top line.

We are seeing this play out in real-time with companies like Block, where CEO Jack Dorsey recently announced massive workforce cuts—nearly 40% of the staff—citing AI-driven efficiencies. If companies need fewer people to do the same amount of work, they need fewer software licenses. This isn't a "breather" for the sector; it is a structural de-rating.

The Anthropic Effect and the Rise of the "Native" Competitor

While the incumbents were busy rebranding their old features with "AI" suffixes, the landscape shifted. The recent sell-off was accelerated by the launch of Anthropic’s Claude Code Security, a tool that doesn't just "help" developers—it scans, identifies, and fixes vulnerabilities autonomously.

This sent shockwaves through the cybersecurity sector. Firms like CrowdStrike and Palo Alto Networks, which built empires on complex, human-monitored security stacks, suddenly look like they are defending a fortress against a fleet of drones.

The investigative reality is that many "legacy" SaaS firms are trapped in a Product-Market Mismatch. They are trying to sell a tool built for a human-centric workflow to a world that is rapidly moving toward an agentic workflow. In an agentic world, the "user interface" isn't a dashboard; it’s an API. If you are still selling dashboards, you are selling a horse and buggy to a trucker.

The Valuation Reckoning

The numbers tell a story of a market that has lost its patience. Look at the compression of Price-to-Earnings (P/E) ratios across the industry leaders:

| Company | 2021 Peak P/E | Early 2026 P/E | Decline % |

|---|---|---|---|

| Adobe | 61x | 18x | 70% |

| ServiceNow | 560x | 77x | 86% |

| Salesforce | 200x+ | 30x | 85% |

Data based on recent market performance and historical peaks.

This isn't just a "tech sell-off." The S&P 500 has remained relatively flat, while the iShares Expanded Tech-Software Sector ETF has plummeted over 27% year-to-date. This is a targeted surgical strike on a specific business model.

Jim Cramer and the Counter-Narrative of Resilience

Not everyone is ready to write the obituary. Jim Cramer, the veteran market observer, has emerged as a vocal critic of the "AI doomsday" scenario. His argument is grounded in the "Pioneers and Infrastructure" thesis. Cramer suggests that while the mid-tier SaaS players might be in trouble, the companies providing the essential "plumbing" for the AI era remain indispensable.

He specifically points to Cadence Design Systems, which provides the software necessary to design the very chips that power AI. You can't have an AI revolution without the silicon, and you can't have the silicon without Cadence.

Cramer’s "playbook" for this sell-off is selective buying. He argues that the market is throwing the baby out with the bathwater, punishing high-quality "compounders" like ServiceNow—which still boasts 20% subscription growth—alongside the truly vulnerable point solutions.

The "Ghost GDP" and the Margin Trap

There is a darker undercurrent to this sell-off that few are discussing openly: the "Ghost GDP" phenomenon. This is a scenario where productivity and headline GDP growth remain high due to AI automation, but consumer spending and employment crater.

If AI-driven white-collar job losses accelerate, as some analysts predict, we could see a massive contraction in the "consumption engine" that drives 70% of the U.S. economy. For software companies, this is a double-edged sword. On one hand, their tools are more valuable than ever because they provide the automation. On the other hand, their customer base—the companies paying for those tools—is shrinking or facing its own budget crises.

Furthermore, the cost of running these AI models is not trivial. Unlike traditional software, where the marginal cost of a new user is near zero, AI features have high compute costs. Vendors are stuck. They have to include AI to stay relevant, but if they don't hike prices, their margins get crushed. If they do hike prices, they risk driving customers toward cheaper, "AI-native" startups that don't have the baggage of a legacy payroll.

Survival of the Most Integrated

The companies that will survive this "SaaSpocalypse" are those moving away from point solutions toward Unified Platforms.

- Vendor Consolidation: IT departments are exhausted by managing dozens of different SaaS contracts. They want one platform that does it all.

- Consumption-Based Pricing: The shift from "seats" to "value" is mandatory. If an AI agent completes a task, the vendor gets paid for the task, not the user who clicked "start."

- Data Sovereignty: The real moat in 2026 isn't the software; it's the data. Companies like Salesforce are betting everything on "Agentforce," claiming their deep repositories of customer data make their AI more effective than a generic model.

The brutal truth is that many of the software "darlings" of the last decade were simply features disguised as companies. AI is now stripping away that disguise. The current sell-off isn't an irrational panic; it's the sound of the market finally demanding that software prove its value in a world where code is becoming a commodity.

We are witnessing a "technical reset" of the highest order. The era of easy growth is dead. What follows will be a lean, high-stakes battle for the "intelligence layer" of the modern corporation. Investors who can distinguish between a dying "seat-tax" model and a thriving "intelligence-utility" model will find the opportunities of a lifetime in the wreckage.

Would you like me to analyze the specific AI roadmaps of the "Big Three" (Salesforce, Adobe, ServiceNow) to see which one has the most viable defense against seat-count erosion?