The mail arrives at 4:00 PM, a stack of glossy envelopes that look like invitations but feel like threats. For Sarah, a thirty-four-year-old dental hygienist in Columbus, the ritual is always the same. She sifts through the grocery store circulars and the water bill until she finds it: the pre-approved personal loan offer.

It promises "financial breathing room" with the upbeat tone of a yoga instructor. It suggests a "fresh start" at a fixed rate. To the casual observer, Sarah is the picture of middle-class stability. She has a reliable SUV, a three-bedroom suburban home, and a steady paycheck. But Sarah is drowning in the shallow end. For an alternative view, check out: this related article.

The grocery bills have crept up by thirty percent. The electricity costs more just to keep the lights at the same dimness. Her credit cards, once reserved for emergencies, became the bridge she crossed every month to reach payday. Now, that bridge is crumbling under eighteen-percent interest rates.

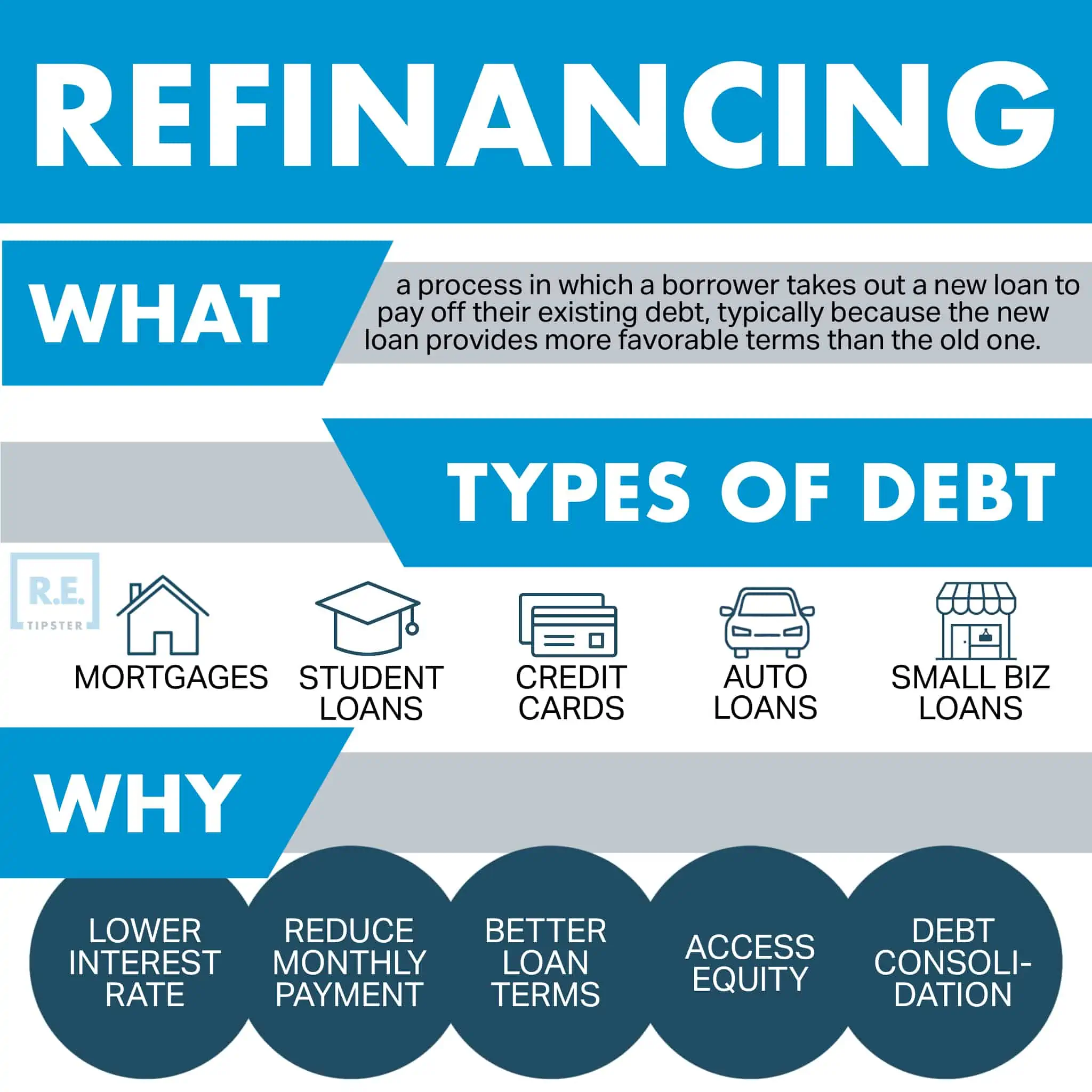

Sarah is the new face of a national surge. Personal loans are no longer just for the desperate or the reckless; they have become the "middle-class refinancing option." When the cost of existing becomes more expensive than the money coming in, people don't just stop buying. They pivot. Similar analysis on the subject has been shared by MarketWatch.

The Math of the Breaking Point

We are witnessing a structural shift in how the average household manages its survival. Recent data shows personal loan originations climbing to record highs, even as interest rates remain stubbornly elevated. It seems counterintuitive. Why would anyone take on more debt when money is so expensive to borrow?

The answer lives in the gap between a credit card’s revolving door and the personal loan’s fixed exit.

Consider a hypothetical scenario involving two neighbors, Mark and Elena. Mark carries $15,000 in debt on a standard credit card with a variable APR of 22%. He pays the minimums, but the interest compounds daily, a mathematical hydra that grows two heads for every one he cuts off. Elena has the same $15,000 debt, but she takes out a personal loan at 12% to pay off the cards.

Elena hasn't actually reduced her debt. She has simply changed its shape. She has moved from a liquid, unpredictable ocean of high-interest revolving credit to a solid, predictable block of installment debt. For the American middle class, "predictable" is currently the most valuable currency on the market.

The Affordability Mirage

The surge in these loans is a symptom of a deeper fever. Wages have grown, but they are sprinting against an Olympic-level inflation rate that started years ago and refuses to sit down. When the price of eggs, insurance, and childcare all hit a local maximum simultaneously, the household budget snaps.

Economists call this "affordability struggles." Sarah calls it "the Tuesday before payday."

The psychological weight of a credit card balance is different from an installment loan. A credit card is a lingering ghost; it follows you. A personal loan feels like a contract with a finish line. This is why the middle class is flocking to them. They are trying to buy time. They are betting that if they can just lock in a monthly payment they can afford today, they can outrun the rising costs of tomorrow.

But there is a hidden gear in this machine. Personal loans are often unsecured, meaning they aren't backed by a house or a car. The bank is betting on your future labor. When thousands of people make this bet at once, it creates a massive, invisible web of obligations that ties the workforce to their desks more tightly than any company loyalty program ever could.

The Ghost in the FICO Score

We are told that a high credit score is the key to the kingdom. What they don't tell you is that the kingdom is built on the very debt you’re trying to manage.

The irony of the current surge is that the "prime" borrowers—those with the best scores—are the ones driving the growth. These aren't people living on the margins; these are people with 720 scores who are tired of watching their disposable income vanish into the pockets of credit card issuers.

The personal loan offers a momentary dopamine hit. You click "accept," the money hits your account, and you pay off three credit cards in a single afternoon. For a few hours, you feel rich. You feel disciplined. You feel like you’ve won.

The danger lies in the empty space left behind on those credit cards. Without a fundamental change in the cost of living or a significant jump in income, that available credit becomes a siren song. If Sarah uses a loan to clear her cards, but the price of groceries continues to outpace her raises, she will eventually reach for the plastic again. Now, she has the loan payment and the new credit card balance.

This is how the "middle-class refinance" turns into a debt trap with a nicer coat of paint.

The Invisible Stakes

Why does this matter to someone who doesn't have a loan? Because credit is the nervous system of our economy. When the middle class begins to restructure its debt en masse, it signals that the old ways of consuming are no longer sustainable.

We are moving away from a society that buys things with money it has, past a society that buys things with money it expects to have, and toward a society that borrows just to maintain the things it already bought.

The stakes are not just financial. They are emotional. There is a specific kind of exhaustion that comes from realizing your entire life is a series of monthly installments. It changes how you see your job. It changes how you see your future. You stop dreaming about what you want to do and start calculating what you have to do.

The "surge" the headlines talk about is actually a collective gasp for air. It is millions of people like Sarah looking at a spreadsheet and realizing that the math of 2024 does not look like the math of 2019.

The Architecture of the Pivot

To understand the rise of these loans, you have to look at the lenders. They aren't the marble-pillared banks of the past. They are fintech companies—algorithms dressed in sleek user interfaces. They make borrowing feel like ordering a pizza.

One-click approvals.

Instant verification.

Funds in your account by morning.

This frictionless borrowing is a feat of engineering, but it removes the "pain of paying" that historically kept debt in check. When the struggle to afford life meets the ease of digital borrowing, the result is an explosion of personal debt that feels almost weightless until the first payment is due.

The reality of the "middle-class refinance" is that it is a sophisticated survival strategy. It is an admission that the standard toolkit of the American dream—work hard, save money, pay your bills—is currently missing a few pieces.

Sarah sits at her kitchen table, the light from her laptop reflecting in her eyes. She looks at the personal loan offer one last time. It’s a 13% interest rate. Her cards are at 24%. It makes sense. It’s logical. It’s the smart move.

She clicks "Apply."

She isn't looking for a luxury vacation or a new home theater. She just wants to be able to sleep through the night without doing mental long division about her debt. She wants to believe that by restructuring her struggle, she can eventually end it.

The loan is a bridge. Everyone is just hoping it’s long enough to reach the other side of an increasingly expensive world.

The quiet click of the mouse is the sound of another American household betting on a future that hasn't arrived yet, funded by a past they are still trying to pay off.

The mailbox will be empty tomorrow, but the weight will still be there, just distributed differently.

Would you like me to look into the specific interest rate trends for different credit tiers to see how they compare to these personal loan offers?