The average American credit score is currently sitting at a "healthy" 701 according to VantageScore. Most financial analysts are popping champagne. They see a resilient consumer. They see stability. They see a soft landing.

They are looking at a rearview mirror while driving toward a cliff.

The narrative that high-income earners are merely "masking" distress for the rest of the population is a shallow observation that misses the structural rot beneath the surface. It isn't just that the wealthy are propping up the averages; it is that the very metrics we use to measure financial health—the FICO and VantageScore models—have become lagging indicators that are fundamentally broken in a high-interest, post-inflationary world.

If you think a 700 score means the economy is safe, you don't understand how debt works in 2024.

The Mirage of the 700 Club

The CEO of VantageScore, Silvio Tavares, recently pointed out that while the average score remains high, there is a widening gap. He’s right about the gap, but he’s wrong about what it signifies. The industry obsession with the "average" score is a classic case of the Flaw of Averages. If I have my head in an oven and my feet in an ice bucket, on average, my temperature is just fine.

But the real danger isn't the statistical spread. It’s the velocity of credit degradation.

Credit scores are historical artifacts. They tell us how well a consumer managed their debt six months ago. They do not reflect the reality of a paycheck that no longer covers the rent, the utility bill, and the $400 grocery run. We are seeing a phenomenon where consumers are maintaining their credit scores at the expense of their actual solvency.

I have watched individuals max out three different credit cards to pay for basic necessities, all while maintaining a "Good" rating because they are making the minimum payments. They are technically "healthy" according to the algorithms, but they are functionally bankrupt.

Why the "High Earner" Shield is a Myth

The prevailing theory is that the $100k+ crowd is the only thing keeping the ship afloat. The logic goes like this: high earners have enough cushion to absorb price hikes, so their pristine scores keep the national average looking pretty.

This ignores the reality of lifestyle creep and debt-servicing ratios.

A high income does not equate to a high net worth or even high liquidity. In fact, some of the most precarious financial positions I’ve audited belong to households making $150,000 a year with $145,000 in annual obligations. When the cost of their variable-rate debt or their HELOC (Home Equity Line of Credit) jumps by 300 basis points, that "cushion" evaporates.

These high earners aren't masking the distress of the poor; they are the next domino to fall. When the upper-middle class stops spending because their debt-to-income ratio hits a breaking point, the service economy—which employs the lower-income bracket—shudders. The "mask" isn't just hiding a problem; it's hiding the scale of the contagion.

The Hidden Math of Default Rates

Let’s look at the numbers the bank PR departments won't talk about. While the average score is 701, the rate of credit card delinquencies is climbing at the fastest pace since the 2008 Great Financial Crisis.

If the scores are high but the defaults are rising, what does that tell you?

It tells you the scoring models are lagging behind reality.

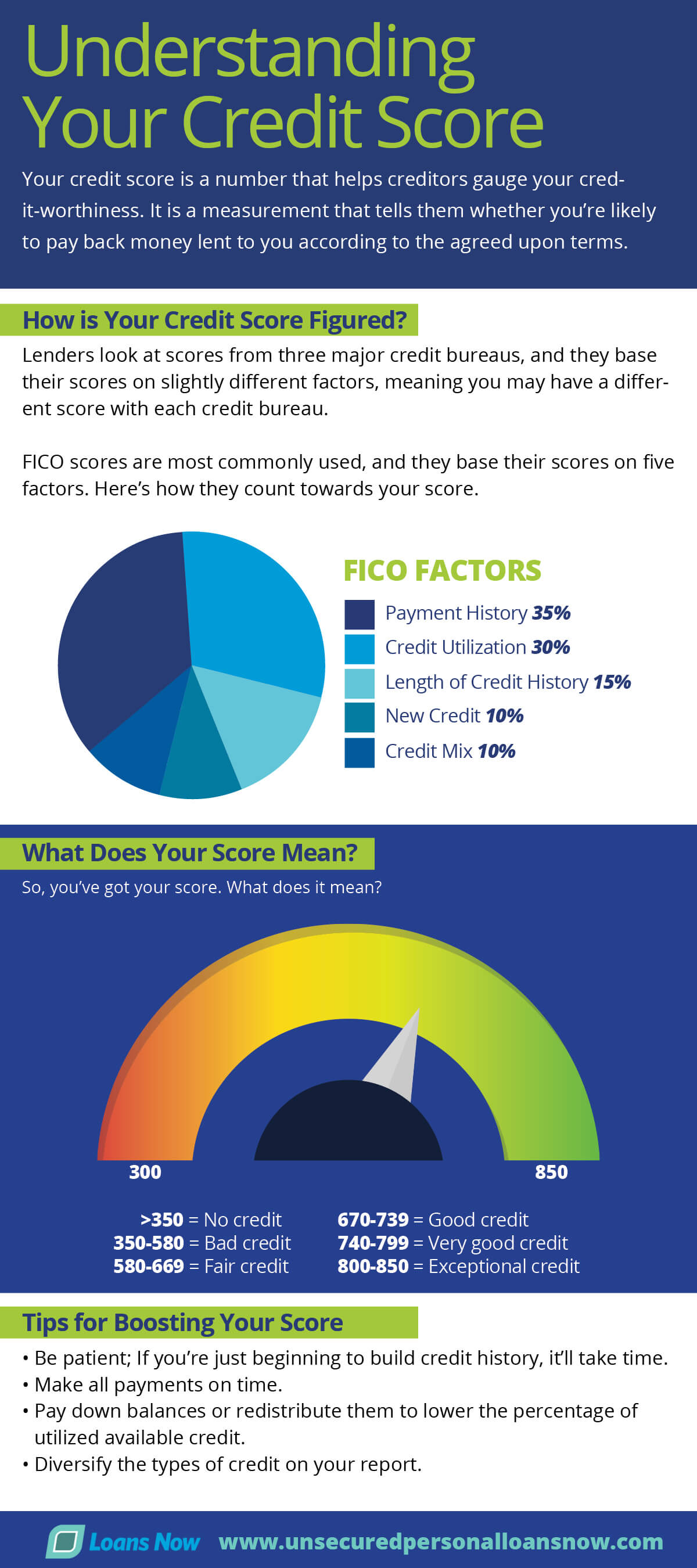

The traditional formula for credit health is roughly:

- 35% Payment History

- 30% Amounts Owed (Utilization)

- 15% Length of Credit History

- 10% New Credit

- 10% Credit Mix

The problem is the Utilization metric. In an era of record-high interest rates (20% to 30% APR on cards), the "Amounts Owed" section becomes a death trap. A consumer can have a low utilization rate today, but because interest is compounding so aggressively, they can hit a debt-spiral threshold within 90 days. The credit score won't reflect the danger until the consumer has already missed a payment.

By the time the score drops, the person is already underwater.

The "Buy Now, Pay Later" Shadow Debt

There is a massive, unregulated monster under the bed that VantageScore and FICO are barely tracking: Buy Now, Pay Later (BNPL).

Services like Affirm, Klarna, and Afterpay have exploded. Millions of Americans are using these "pay-in-four" installments for everything from Peloton bikes to groceries. Much of this debt does not report to the major bureaus unless it goes to collections.

This means the "average" credit score is missing a significant portion of the consumer's total debt load. We are essentially looking at a balance sheet where half the liabilities are hidden off-book.

Imagine a scenario where a consumer has a 720 score. They have two credit cards with 20% utilization. Looks great. But they also have six active BNPL plans that consume 40% of their monthly take-home pay. On paper, they are a prime borrower. In reality, they are one flat tire away from a total financial collapse.

Stop Chasing the Number

If you are a consumer, the worst thing you can do right now is optimize for a score.

The score is a tool for the lender to extract interest from you. It is not a measurement of your wealth. I’ve seen people with 800 scores who are broke, and people with 600 scores who have $2 million in the bank because they refuse to play the credit game.

The status quo advice is to "keep accounts open" and "never close a card" to maintain your score's age. This is often terrible advice for someone staring down a debt crisis. If a card is an open invitation to spend money you don't have at a 24% interest rate, the "hit" to your credit score for closing it is a small price to pay for your financial sanity.

The Liquidity Trap

The real metric you should be watching isn't your VantageScore; it’s your Cash-to-Debt Service Ratio.

$$\text{CDSR} = \frac{\text{Monthly Disposable Income}}{\text{Total Monthly Debt Obligations}}$$

If this ratio is shrinking, you are in trouble, regardless of what the three bureaus say.

The "healthy" average we see in the news is a lagging indicator of a consumer base that has run out of runway. The stimulus money is gone. The student loan pause is over. Savings rates are at historic lows. Credit card balances have crossed the $1 trillion mark.

The CEO of VantageScore is essentially telling you the weather is fine while the barometer is screaming that a hurricane is landing. The high earners are not "masking" the distress; they are simply the last ones to feel the water rising around their necks.

Burn the Playbook

The banks want you to care about your score because it keeps you in the ecosystem. It keeps you eligible for the next consolidation loan, the next balance transfer, and the next high-interest trap.

Stop looking at the average. The average is a lie.

The reality is that we are witnessing the Great Decoupling. The gap between "Credit Health" (as defined by an algorithm) and "Financial Survival" (as defined by your bank balance) has never been wider.

If you are waiting for the average credit score to drop before you admit the economy is in trouble, you’ve already lost. The collapse won't be televised in the form of a 650 average; it will happen in the form of millions of 700-score consumers who can no longer afford to buy bread.

Close the apps. Ignore the "Good" rating on your dashboard. Look at your cash flow. That is the only score that matters. Everything else is just marketing for the debt industry.