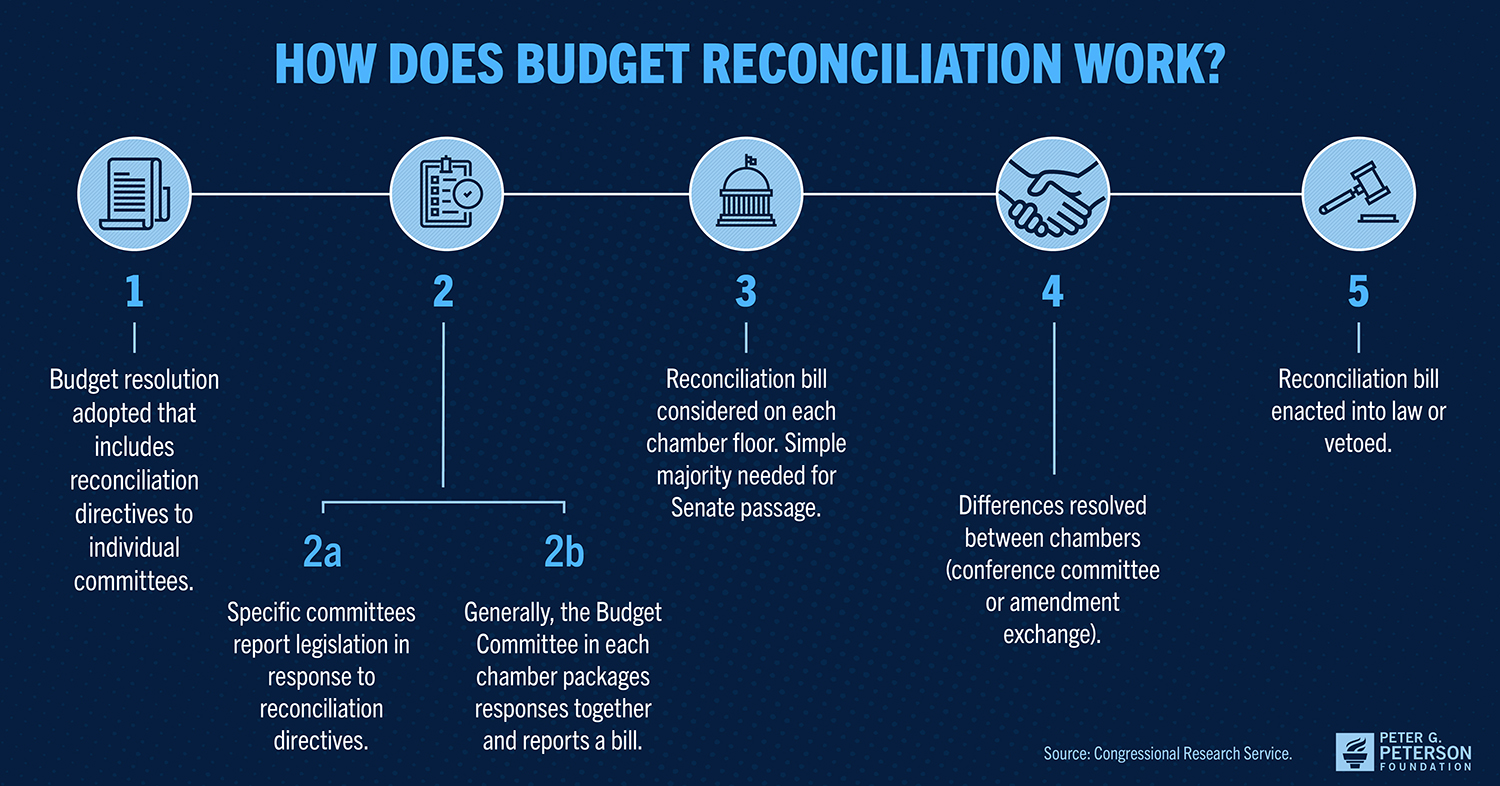

The proposed expansion of tax cuts under a second Trump administration hinges not on broad legislative consensus, but on the mechanical exploitation of budget reconciliation. This fiscal tool allows the Senate to bypass the 60-vote filibuster threshold, moving legislation with a simple majority. However, the efficacy of this strategy is constrained by the "Byrd Rule," which prohibits provisions that do not have a direct, non-incidental impact on the federal budget or that increase the deficit beyond a ten-year window. The feasibility of new tax cuts depends entirely on the interplay between three variables: the baseline expiration of the Tax Cuts and Jobs Act (TCJA) of 2017, the specific growth-multiplier assumptions used by the Congressional Budget Office (CBO), and the availability of "offsets" through tariff revenue or spending reductions.

The Structural Expiration of TCJA and the Revenue Baseline

A central driver for this upcoming legislative push is the looming sunset of key TCJA provisions at the end of 2025. Without intervention, individual income tax rates will revert to 2017 levels, the standard deduction will be halved, and the $10,000 cap on State and Local Tax (SALT) deductions will disappear. For an alternative perspective, check out: this related article.

The strategy currently under development treats this expiration not as a crisis, but as a legislative vehicle. By folding new tax cut proposals into a "TCJA Extension" reconciliation bill, the administration can frame the fiscal impact relative to a "current policy" baseline rather than a "current law" baseline. This distinction is vital for parliamentary compliance. Under a current law baseline, extending the cuts is scored as a multi-trillion-dollar cost; under a current policy baseline, it is the status quo. The administration’s goal is to lower the corporate tax rate further—potentially from 21% to 15%—while simultaneously making the individual protections permanent.

The Three Pillars of the Reconciliation Strategy

The architecture of the proposed tax plan rests on three distinct logical pillars designed to satisfy the procedural requirements of the Senate Parliamentarian while maximizing economic signaling. Further coverage regarding this has been provided by Reuters Business.

1. The Corporate Rate Delta

Reducing the corporate statutory rate from 21% to 15% is the primary supply-side objective. The logic follows the "Capital Depth Hypothesis," which posits that lower corporate tax burdens increase the after-tax return on investment, leading to higher capital expenditures (CapEx). From a strategic consulting perspective, the 15% target is specifically chosen to align the United States with the OECD Global Minimum Tax agreement's floor, effectively neutralizing the incentive for multinational corporations to shift profits to low-tax jurisdictions.

2. Full Expensing (Section 168(k))

A critical component of the proposal is the restoration of "bonus depreciation" or 100% full expensing for short-lived capital assets. Under current law, this benefit is phasing out. By allowing businesses to immediately deduct the full cost of equipment and machinery purchases rather than depreciating them over years, the policy shifts the tax burden away from investment and toward consumption. This creates a powerful short-term stimulus for the manufacturing and industrial sectors.

3. Tariff-Revenue Coupling

Unlike the 2017 tax cuts, which were largely deficit-financed, the 2026 iteration seeks to utilize aggressive tariff regimes—specifically a baseline global tariff and targeted China-specific duties—as a revenue offset. This creates a "Dual-Effect Feedback Loop":

- Revenue Generation: Tariffs act as a consumption tax on imports, providing a cash inflow that can technically "pay for" the reduction in income or corporate taxes within the ten-year reconciliation window.

- Protectionist Re-Shoring: The increased cost of imports, combined with a lower domestic corporate rate, is intended to bridge the cost-parity gap for domestic manufacturing.

The Cost Function and the Byrd Rule Constraint

The primary threat to this strategy is the "prohibited deficit increase" clause. If the CBO determines that the tax cuts will increase the long-term deficit (beyond year 10), the provisions must sunset. This leads to "The fiscal cliff paradox": the more permanent the tax cuts appear, the harder they are to pass under reconciliation rules.

To bypass this, the administration must either find massive spending cuts or utilize "dynamic scoring." Dynamic scoring assumes that the tax cuts will generate enough economic growth to partially pay for themselves through a broader tax base. However, the elasticity of taxable income is a contested variable. If the growth multiplier is lower than anticipated (e.g., $0.40 in revenue for every $1.00 cut), the bill will require deeper cuts to the "non-defense discretionary" budget to remain Byrd-compliant.

Execution Risks and Operational Bottlenecks

Even with a unified government, three bottlenecks remain that could derail the scope of the tax cuts.

The SALT Cap Leverage Point:

Republicans in high-tax states (New York, New Jersey, California) face significant political pressure to repeal the $10,000 SALT cap. Repealing the cap is expensive, potentially costing $100 billion per year in lost revenue. This creates an internal party trade-off: a legislator must choose between a lower corporate rate or tax relief for their specific suburban constituents.

The Interest Rate Sensitivity:

The 2017 tax cuts were enacted in a low-interest-rate environment. In 2026, the cost of servicing the national debt is significantly higher. If the market perceives the tax cuts as inflationary, the Federal Reserve may maintain higher interest rates, which increases the "crowding out" effect. Higher borrowing costs for the private sector could effectively cancel out the investment incentives provided by the 15% corporate tax rate.

The Parliamentarian’s Veto:

The Senate Parliamentarian has the authority to strike "extraneous" provisions. If the administration tries to include non-fiscal policy goals—such as energy deregulation or labor reform—within the tax bill, they risk a "Byrd-ing" of the legislation, where the most impactful sections are stripped out on the Senate floor.

Quantification of Macroeconomic Assumptions

A rigorous analysis of the proposal requires a breakdown of the projected fiscal impact over a standard ten-year window. Based on historical data from the TCJA and current CBO projections, the following estimates provide a framework for the plan’s scale:

- Extension of Individual Provisions: ~$3.5 Trillion to $4.0 Trillion.

- Corporate Rate Reduction (21% to 15%): ~$600 Billion to $800 Billion.

- Interest Expense (Debt Service): Adds approximately 15-20% to the total cost over the decade.

- Tariff Revenue Offset: Potentially $2.0 Trillion to $3.0 Trillion, depending on the elasticity of import demand.

The net fiscal gap—the amount that must be covered by spending cuts or growth—ranges between $1.5 Trillion and $2.5 Trillion.

Strategic Asset Allocation Under a Reconciliation Regime

For corporations and institutional investors, the "Reconciliation Regime" necessitates a specific tactical playbook. The shift toward a 15% corporate rate and 100% expensing prioritizes capital-intensive industries over service-oriented ones.

- Front-Loading CapEx: Companies should prepare to accelerate machinery and technology procurement to coincide with the restoration of 100% bonus depreciation.

- Supply Chain Recalibration: Given the reliance on tariffs to fund the tax cuts, the net benefit of a lower tax rate may be negated for firms with high import dependencies. A "Tax-Tariff Neutrality" audit is required to determine if the tax savings exceed the increased Cost of Goods Sold (COGS) from duties.

- Capital Structure Optimization: If the tax cuts lead to higher interest rates, the relative advantage of debt financing decreases. Firms should look to deleverage while the corporate rate is high and transition to equity-based growth strategies as the 15% rate takes effect.

The most effective play for a firm is to pivot toward domestic production models that maximize the deduction for foreign-derived intangible income (FDII) while utilizing the full expensing of domestic assets. This aligns the corporate balance sheet with the administration's stated objective of domestic industrial expansion while hedging against the inflationary pressure of deficit-financed tax policy.

Would you like me to develop a comparative table mapping the projected tax liabilities of a Fortune 500 manufacturing firm versus a tech-service firm under this 15% rate and tariff-offset scenario?